Carrier Q4 2024 financials are out

The nation’s top three wireless service operators released the results of their busy holiday quarter. Here is Circana’s quick take on the major trends coming out of their Q4 performances:

T-Mobile’s postpaid rocket continues to soar:

T-Mobile once again led the industry with the addition of 903K new postpaid phone lines, up from 850K in the year-ago quarter. The carrier noted that 160K of these new postpaid users were not new to the T-Mobile network, as they migrated over from the Metro prepaid service. Despite this migration, T-Mobile managed to grow its prepaid base by 103K, maintaining its lead in the prepaid segment with over 25 million customers. The revenue impact of the Mint Mobile acquisition remains mixed, as prepaid ARPU declined again (from $35.94 in Q2 2024 to $34.88 in Q4 2024) given Mint Mobile’s low-cost positioning. However, postpaid ARPU remained steady thanks to the strong adoption of premium plans and enterprise expansion.

Verizon’s value proposition pays off:

Verizon’s postpaid phone net adds continues to gradually improve, with the carrier adding 568K new users, up from 449K in the year-ago quarter. Notably, 428K of these new additions were consumer phone lines, up from 318K a year ago. In fact, Q4 2024 marks the first quarter in three years when Verizon enjoyed consecutive gains in consumer postpaid phone activations. As in the last quarter of 2023, Verizon added over 700K of net connected devices thanks to strong promotions on connected iPads and Apple Watch smartwatches bundled for free with new iPhone activations for new and existing customers. It is noteworthy to highlight that the generous subsidies were instrumental in this strong Q4 performance, but the carrier had to give up on margins to make this happen as its equipment revenue costs jumped 5% from the year-ago-quarter. Verizon also had a strong performance in prepaid as its “value” marketing efforts centered around the (re-branded) Total Wireless and digital-only Visible brands resonate with cost-conscious users. Excluding the Lifeline brand Safelink net losses driven by Affordable Connectivity Program (ACP)-related deactivations, Verizon’s reported positive prepaid net adds for the second quarter in a row (80K in Q3 2024 and 65K in Q4 2024). This is a major accomplishment considering that the carrier lost over 1.2 million prepaid connections (excluding Safelink) in the past six consecutive quarters prior to Q3 2024.

AT&T maintains the strong momentum:

AT&T had another strong quarter, adding 482K new postpaid phone subscribers, though this figure was slightly down from 526K in the year-ago quarter. Like other rivals, AT&T’s postpaid ARPU hit an all-time high thanks to persistent efforts to move legacy plan customers on to higher tier rate plans alongside gradual rate hikes across the board. Some of the ARPU growth can also be attributed to the carrier’s attractive promotions on connected devices (e.g. free iPad or Apple Watch SE with purchase of new iPhone 16) that generate additional monthly revenue per each activated device. By contrast, the carrier’s prepaid base contracted for the second quarter in a row as it lost 138K prepaid connections (almost the same as in Q4 2023). Nevertheless, AT&T continues to lead the market in prepaid churn.

Long-awaited inflection point in device upgrades:

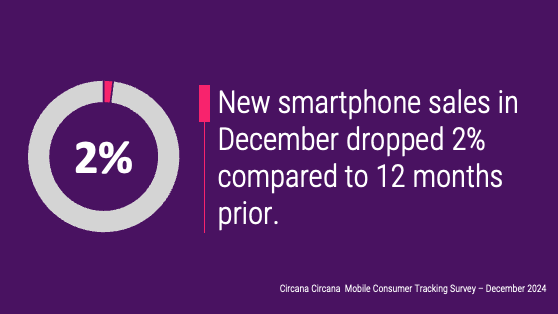

According to the Circana Mobile Consumer Track, new smartphone sales in December declined 2% year over year. However, this was a notable improvement over the previous months, where volumes had been averaging a 10% decline year over year. As we highlighted in earlier analyses, the smartphone market has been grappling with a fundamental shift in replacement cycles, driven by a lack of breakthrough innovation and persistent macroeconomic pressures, prompting consumers to hold onto their devices longer. We have long anticipated an inflection point in the replacement cycle due to the record age of the installed smartphone base, and Circana’s December data, alongside carriers’ newly reported postpaid upgrade rates, indicate that we are finally there. T-Mobile’s postpaid device upgrade rate jumped from 3.2% in Q4 2023 to 3.6% in Q4 2024; AT&T continued to lead the market with the same 6.2% upgrade rate as in Q3 2024; and Verizon’s upgrade rate slightly inched up from 4.4% in Q3 2023 to 4.5% in Q4 2024. Notably, carriers’ strong upgrade deals including the aforementioned connected device bundles was the main driver of this growth in replacements.

FWA activations remain strong:

T-Mobile and Verizon’s 5G-based FWA Home Internet services continue to expand, though growth rates are slowing. T-Mobile added 428K new FWA connections in Q4 2024, down from 541K in Q4 2023, reflecting the impact of pricing adjustments made earlier in the year as well as the limitations with network capacity. Verizon, meanwhile, added 373K new FWA subscribers in Q4, slightly down from 375K in Q4 of last year. AT&T, which entered the FWA market in Q3 2023, added more double the number of FWA connections in Q4 2024 (158K vs 67K in Q4 2023) despite little effort. AT&T has long been vocal about its long-term fiber expansion strategy, which is on track with its guidance as the carrier continue to add between 230K to 300K new consumer fiber accounts in each tracked quarter. While FWA remains a critical growth area, increasing capacity constraints may continue to limit expansion in 2025, particularly for T-Mobile and Verizon, which are nearing saturation in key markets.