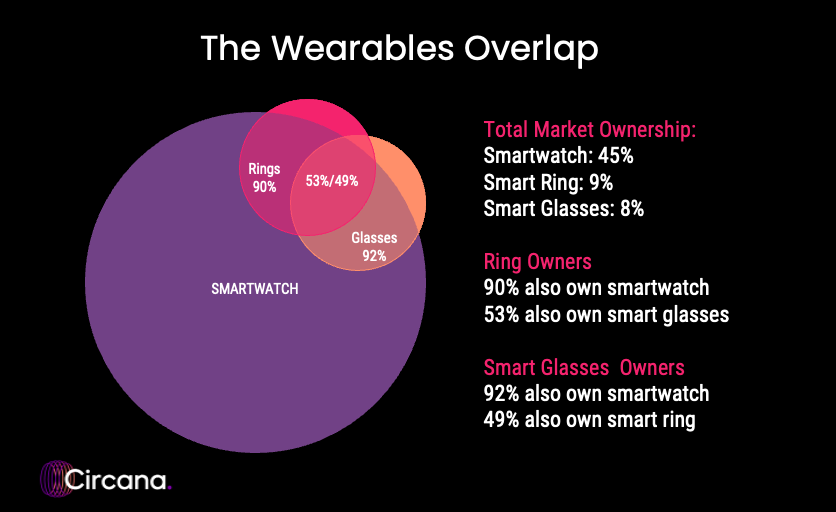

The wearables market appears to have a problem: the only consumers who are interested in the latest and greatest tech are the ones who have already committed to the category. Take smart rings, for example: just 10% of smart ring owners do not already own (and use) a smartwatch which suggests that they view the smart ring as a complement to the watch, rather than the replacement it was supposed to be. The same applies to smart glasses, where just 8% of smart glasses owners do not also own a smartwatch. Even more interesting, perhaps, is the overlap between smart ring and smart glasses owners, with roughly 50% of said owners committing to both new technologies.

This is, in many ways, good news for smartwatch manufacturers as they are clearly not at risk of being replaced by these newer technologies any time soon. But it’s more concerning for the newer tech, which appears to be constrained by the size of the smartwatch market. That’s not terrible – an estimated 45% of the US adult population owns a smartwatch – but it’s also not great for two new device types that should be able to survive beyond the smartwatch constraint.

The smart ring limitation is easier to explain. The ring is focused on health and wellness primarily, looking to serve up data stats about you that are more accurate, and exceed, those provided by a smartwatch. The challenge is that the smartwatch already tracks a broad range of health and wellness data so there’s not much incremental data to be harvested. That means the ring has to focus on being even better than the watch, which will only appeal to a relatively small set of consumers. The better use case is as a complementary device, using the ring for sleep tracking while the smartwatch charges (as an aside, many consumers don’t want to wear a bulky watch at night anyway). However, only 38% of smartwatch owners appear to care about sleep tracking so this could limit the size of the smart ring market to just a third of the smartwatch base… and that’s before you factor in other deterrents such as being yet another device to charge, another interface that tracks the data (and potentially, another service fee to actually get the detailed data results).

Smart glasses are a less obvious overlap: they do not try to replicate the health and fitness features of a watch or ring and should target a different – social media focused – audience. The reason for the overlap here is more likely to be one of the early adopter market: the same consumers who were early to buy into the smartwatch are a similar breed to the ones that are interested – at least initially – in smart glasses. As such, we think that smart glasses have the potential to expand further beyond the smartwatch “bubble” to create a distinct audience.

But back to the health and fitness brigade one more time. As we continue to see new variants enter the market, such as rings, or screenless wristbands (think Whoop and upcoming competitors) we do not expect them to attract a new audience. Rather, they will be competing against the current watch incumbents to carve out a share of the market. And with Apple owning roughly 65% of the smartwatch market (and the related loyalty customers have to the Apple ecosystem), that could be a case of ever-diminishing returns.