We’ve just published our latest Broadband America report, which examines the state of internet connectivity across the continental United States. The good news is that more connected homes are seeing broadband speeds, with 84% of connected homes enjoying speeds greater than 25 Mbps, and 65% of these connected homes seeing download speeds greater than 100 Mbps, which is becoming the new threshold definition for broadband.

But there is also a cause for concern – the “Fewer” in the title. By the end of 2024, census data shows that a third of all US counties (roughly 1,000) had fewer homes with an internet connection of any kind than the previous year. It’s a trend that is only noticeable when you zoom into county-level data: when looking at the country as a whole, or even at a state level, the counties that had increased internet connectivity outweighed (in number and speed increases) this negative statistic.

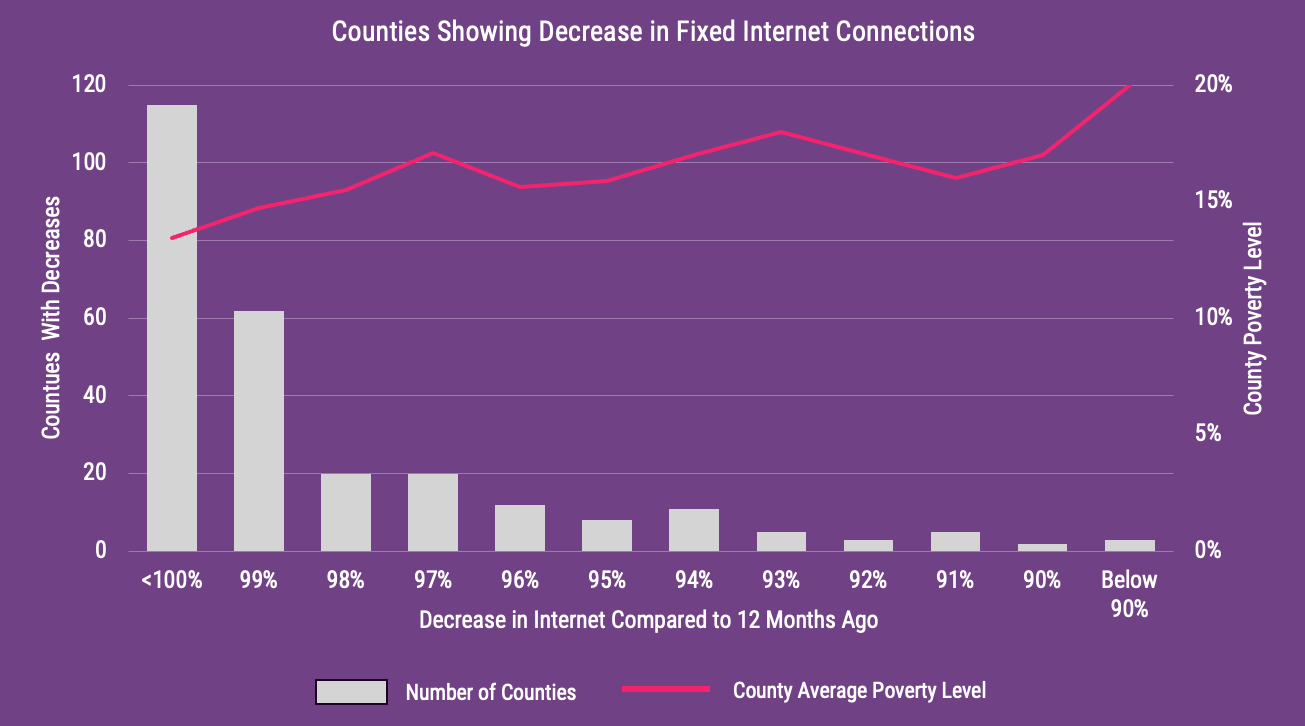

The negative story becomes a little more palatable if we strip out the mobile connections and focus just on fixed internet to the home solutions, but there are still nearly 300 counties – roughly 10% of all counties tracked – that show a reduction in connectivity. Or to look at it another way, a lot of those households that have stepped away from the internet have done so by cancelling their mobile phone service. That is potentially cause for greater concern than the story of fixed internet decreases.

The decrease is almost certainly related to affordability, and it impacts both fixed internet to the home, as well as the mobile service option. The counties where the access decreases are most noticeable are typically ones with a higher poverty level (ranging from 15-25%) as well as being more rural markets, which typically means fewer competitive internet options, leading to higher monthly access fees.

But poverty levels only tell a small fraction of the story: the larger impact is among households that are above the poverty level but still struggling. In these homes, the increased cost of living over the past few years, coupled with the demise of the Affordable Connectivity Program (ACP) – which had 23 million beneficiaries at its peak – have meant that financial compromises need to be made. And Internet access appears to be considered as a “nice to have” rather than a necessity such as food and fuel.

We can expect the situation to potentially get worse: the impact of ACP’s demise is only starting to show up in the 2024 census data: the real impact will show up in next year’s report. So too will the increasing impact of macro-economic factors such as tariffs and increased fuel prices that impact both heating and transportation – again, necessities for households that often require sacrifices elsewhere.

The long (and short) term impact of less internet access is hard to quantify, simply because the impact can be so far reaching. Children cannot complete their schoolwork at home, so they end up camping out in fast food restaurants to complete their work (if there is one nearby – an issue in more rural markets of course), there’s a dearth of current news and other information at hand and, of course, there’s an impact on consumer electronic purchases. No internet means no need for a smart TV or any other so-called “smart” product. There is a direct connection between many consumer tech purchases and the speed of internet in the home (we track this in the Fall Broadband Consumer Report).

Ten years on from when the UN declared Internet access to be a basic human right, the US market looks to be heading in the wrong direction. Let’s hope that’s a short-term blip. The carriers have certainly recognized, and reacted, to the potential issue by focusing on converged solutions (fixed plus mobile) with highly competitive offers, but these solutions face the current macro-economic headwinds that have become stronger in the past 12 months.